When one monitors financial activities – inflows and outflows from company’s bank account, one usually analyses and presents data in table. It’s just something we are used to and basically there is nothing wrong with it. We should have enough time and carefully read through cash flow statements to clearly see what is happening with our most liquid assets. Let’s be honest – at the end, cash is the king and cash is what every business is about  .

.

However, as life is getting faster and faster we often miss the time to carefully read all reports, especially if they consist mainly from tables with lots of data. In such cases the reader needs to really focus, understand and have good analytical skills to get to some meaningful conclusions based on reports. That is why all BI (business intelligence) solutions put more and more effort into providing good and simple options to visualize our data. The reason for this lies in fact that most people are visual types and are thus able to see trends and anomalies from charts faster than from tables. Lots of companies already use different BI solutions with such options and present their business results using different charts.

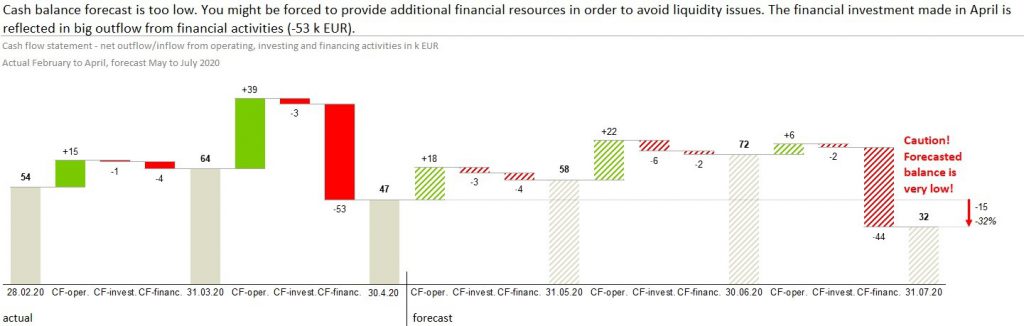

Further, let’s explain green and red bars in between. They present net inflow (green) or outflow (red, obviously ) from different types of business activities.

- Cash flow from operating activities is one generated by company’s core business operations (receivables collection, wages and payables payments).

- Cash flow from investing activities is the one generated from buying or selling equipment, assets or financial investments (for example shares in other companies).

- Cash flow from financing is mainly generated from debt, loans or capital changes.

Chart shown above was created at the beginning of May 2020, when the last actual date was end of April 2020. Left part of chart is presenting past actual data while right side of chart is reserved for presenting forecasted cash flow for next three months. Therefore, forecast bars are striped while bars presenting actual data on the left are coloured fully – so you can immediately see what is actual and what forecasted data. On the very right side of the chart, you can also see red arrow pointing down and two numeric data. These are showing the difference from last actual cash position to last forecasted cash position. The difference is minus 15k EUR which means 32%. It is quite a lot and cash positon in amount 32k EUR is not enough for this company to avoid liquidity issues. Therefore, you can also see red caution alert above the grey bar.

General rule for services companies is that cash position in any point of time should not be less than the amount of three months’ costs.